Gen Z Guide to Financial Independence

Mar. 17, 2026

{kind=link}

Balancing Saving vs. Spending in Your 20s

Gen Z doesn’t want to “just survive.”

You want flexibility. Options. The ability to quit, pivot, travel, build, create, or rest — without money anxiety controlling every move.

The real debate isn’t saving vs. spending.

It’s freedom now vs. freedom later — and how to design both.

Here’s how to think about financial independence in a way that actually fits Gen Z.

The Problem: Old Money Advice Feels Outdated

Most financial advice says:

- Build an emergency fund

- Invest in index funds

- Cut your fun spending

- Retire at 65

That’s not inspiring. And it ignores modern realities:

- Side hustle income

- Career pivots every 2–3 years

- Remote work

- Rising rent

- Social media lifestyle pressure

- Burnout culture

Gen Z needs a different framework.

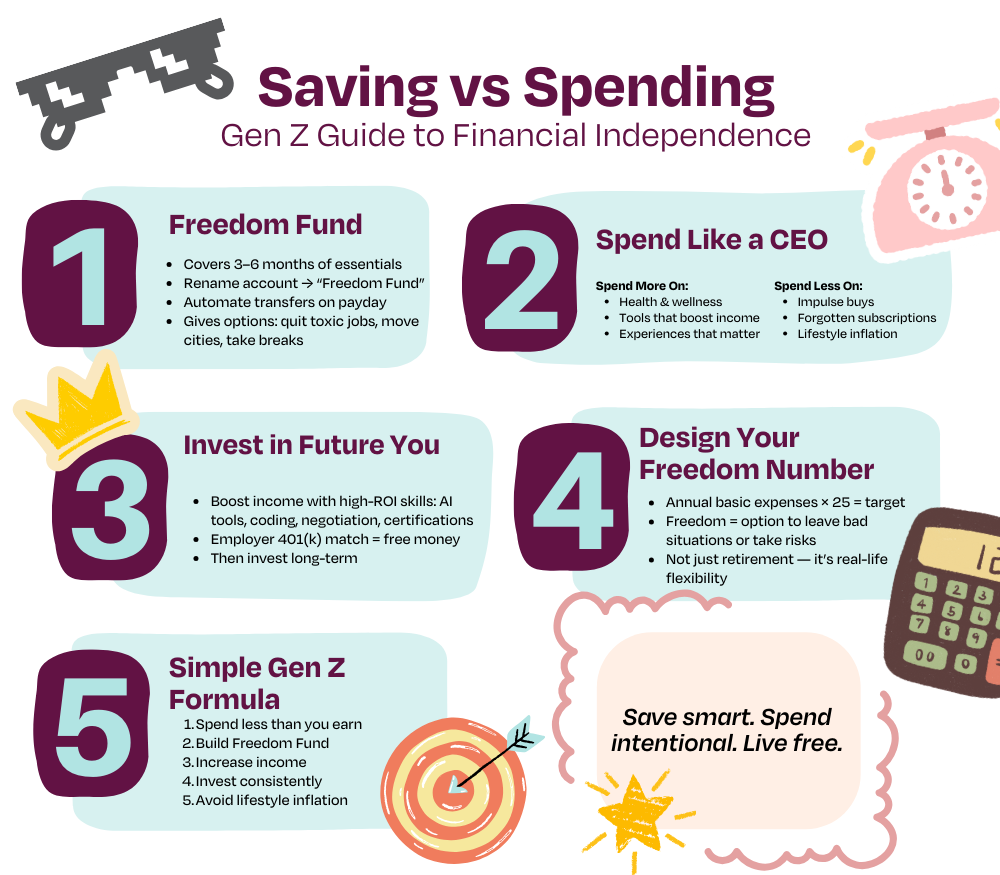

Step 1: Build a “Freedom Fund” (Not an Emergency Fund)

“Emergency fund” sounds like something went wrong.

A Freedom Fund assumes something better is possible. This is money that lets you:

- Quit a toxic job

- Leave a bad relationship or roommate

- Move to a new city

- Take 3 months to upskill

- Start a business idea

- Say no without panic

This isn’t survival money. It’s leverage.

How to Build It:

Calculate your “Walk Away Number” (3–6 months of bare-minimum expenses)

- Open a separate high-yield savings account

- Rename it “Freedom Account”

- Automate transfers on payday

When saving is tied to empowerment, it becomes motivating — not restrictive. Saving = power.

Step 2: Spend Like a CEO, Not a Consumer

Gen Z doesn’t have a spending problem. Gen Z has a comparison problem.

Social media makes lifestyle inflation look normal:

- Constant travel

- Designer everything

- Luxury apartments

- Daily takeout

But here’s the truth: You’re seeing curated highlights — not credit card balances.

Instead of cutting everything, audit your spending like a CEO:

Spend More On:

- Health (therapy, gym, nutrition)

- Tools that increase income

- Networking and career growth

- Experiences you deeply value

Spend Less On:

- Trend-driven impulse buys

- Buy Now, Pay Later traps

- Subscriptions you forgot

- Impressing people you don’t even like

Ask: Does this purchase increase my freedom — or decrease it?

Intentional spending > restrictive budgeting.

Step 3: Invest in “Future You” Before the Stock Market

Yes, investing early matters. But early in your career, your biggest asset isn’t your portfolio. It’s your earning power.

Before obsessing over ETFs, ask: What skill could increase my income by 30–50% in the next 2 years?

High-ROI skills include:

- AI productivity tools

- Coding or data analytics

- Sales and persuasion

- Public speaking

- Negotiation

- Digital marketing

- Industry certifications

A $1,500 course that increases your salary by $10,000/year beats a 7% annual market return. Your income ceiling matters more than your expense cutting.

Smarter Order of Operations:

- Build Freedom Fund

- Get employer 401(k) match (free money)

- Invest in income-growing skills

- Then aggressively invest long-term

Time in the market matters. But so does income acceleration.

Step 4: Design Your “Freedom Number”

Forget retirement at 65.

Ask: How much would I need invested to cover my basic lifestyle? Financial independence isn’t always full retirement. It might mean:

- Covering rent from investments

- Working part-time by 35

- Taking a 1-year sabbatical

- Starting a passion project without pressure

Calculate: Annual basic expenses × 25 = Rough freedom number

(Using the 4% rule as a guideline)

When you know your number, money stops feeling abstract. It becomes a target.

The Real Formula for Gen Z Financial Independence

- Spend less than you earn

- Build a Freedom Fund

- Increase income aggressively

- Invest consistently

- Avoid lifestyle inflation

- Repeat for 10–15 years

Wealth doesn’t usually come from one big win.

It comes from small, consistent decisions.

The Social Media Illusion

Here’s something no one says loudly enough: Looking rich and being financially independent are not the same thing.

Some people:

- Lease cars they can’t afford

- Finance trips

- Carry credit card debt

- Depend on their next paycheck

True wealth is quiet. Financial independence rarely trends on TikTok.

But it changes your life.

The Real Goal: Options

Financial independence isn’t about retiring at 30. It’s about:

- Leaving bad situations quickly

- Taking career risks

- Starting businesses

- Helping family

- Working because you want to — not because you have to

Saving gives you stability. Spending gives you enjoyment. Investing gives you options. Balance all three intentionally.

Gen Z has something powerful:

- Access to global income streams

- Digital tools

- Investing apps

- AI productivity tools

- Remote work flexibility

You don’t need to be perfect with money. You need to be consistent and intentional.

- Start small.

- Increase your income.

- Protect your freedom.

- Invest long-term.

Your 35-year-old self will be grateful you started at 22.

Back-to-School Giveaway 2026

Community

Aug 3, 2026

Don't Let Fake School Supply Deals Drain Your Wallet

Scam Alerts

July 21, 2026